As businesses and governments around the world increasingly seek ways to limit emissions of carbon dioxide in order to reduce the risk of extreme temperatures, heavy industries such as concrete are steadily working to reduce their carbon output – however a number of outlying factors may influence mitigation pathways more profoundly than the options currently available – with the increasing likelihood that the industry may be able to reduce its emissions almost completely.

Concrete manufacture is responsible for approximately 5% of global carbon emissions (road transport is at about 18%), with about 50% of this figure attributed to the use of fossil fuels and 50% to the calcination of limestone, where carbon is ‘burnt off’ to produce calcium oxide, which is blended with other materials to form calcium silicates and other compounds to make cement.

Within Europe, the cement industry is lead by the consortium Cembureau who have recently published a report on the ongoing albeit minor reduction in CO2 output since 2005 in Europe as well as other Cement Sustainability Initiative (CSI) members worldwide; showing that progress is being made. This is followed up by Cembureau’s ‘Low Carbon Economy roadmap‘, which highlights 5 pathways to a 32% reduction of emissions compared to 1990 levels using conventional means, and a further 48% reduction using potential ‘breakthrough’ technologies which would bring emissions in line with Paris Agreement targets. This additional 48% reduction constitutes the bulk of the problem – but it seems as though a solution has emerged that looks capable of bringing about the changes needed in this vast industry to bring emissions down by 80% over 1990 levels – if implemented.

Firstly, to understand the constraints placed on the industry it is worthwhile noting the advantages of conventional cement manufacture. The required raw materials – mostly limestone and energy to reduce the limestone to lime ‘clinker’, is available almost everywhere. Factories are usually built next to quarries because its easier to transport the reduced weight of cement than the limestone itself. However, even before this stage, a number of alternatives are available. The first option is to substitute cement entirely by another binder – in an effort to reduce the 50% of CO2 emitted via the calcination process. And here we find that a number of materials may be used outright instead of conventional limestone. Generally, these materials are either Ground Granulated Blast-Furnace Slag (GGBS), produced as a waste material of the steel industry or Fly Ash, a waste material of the coal industry. These substances both act in the same way as powdered limestone clinker – containing high levels of silicates formed under extreme temperatures. These materials (known as Supplementary Cementitious Materials, or SCMs) are usually used in small quantities as an addition to the cement mix, but are increasingly used to replace the cement constituent of concrete entirely. An Irish company ‘Ecocem’ is now producing a concrete made using solely GGBS, with only 4% of the CO2 output of tradional Portland cement. This is because the material is classified as a waste product, and replaces both CO2 emitting processes required in limestone ‘sintering’; both energy use and reduction of calcium carbonate (limestone) to calcium oxide and CO2.

The problem with the use of these SCMs to substitute limestone clinker is that there are limited supplies around the world, and demand for low-carbon cement alternatives are increasing rapidly. Altogether, this leads to a situation where, as Cembureau lays out in its 5 point low-carbon pathways plan, alternative ways still need to be found.

However, the impetus to both reduce energy use and reduce CO2 process emissions has now been combined with another motivation – to make practical use of potential waste CO2 streams at scale, at an economic price point. This presents a compelling proposition: what if CO2 could be cheaply incorporated into the manufacture of binding materials making up cement – thus providing a revenue stream for the large amounts of CO2 available as a waste stream from many industries.

A number of companies have been engaged in solving this problem, and it seems as though the answer has been found; if it can be commercialised at scale, and within cost.

Solidia Concrete

In a partnership that now spans a number of multinationals including LaFarge, BASF, Air Liquide and Totale, the US company Solidia Technologies have developed a cement alternative that reduces the end-to-end CO2 emissions of concrete by 70%, with higher quality performance, using CO2 rather than water to cure the mineral cement formula. From the Solidia website:

“Solidia Technologies® makes it easy and profitable to use CO2 to create superior and sustainable building materials. Solidia’s patented technology starts with a sustainable cement, cures concrete with CO2 instead of water, reduces carbon emissions up to 70%, and recycles 60 to 100% of the water used in production. Using the same raw materials and existing equipment as traditional concretes, the resulting CO2-cured concrete products are higher performing, cost less to produce, and cure in less than 24 hours.”

With the backing of the most serious industry players as investment partners, it is difficult to disprove the authenticity of the claims made. Solidia has begun commercialising its pre-cast products, which are being made available for sale in 2017.

[media-credit name=”Much of the emissions reduction is a result of the 30% lower temperatures required to create the cement” align=”alignleft” width=”386″] [/media-credit]

[/media-credit]

In reality, while the claims certainly present a great development for the industry, some limitations may appear when considering the industry as whole. First of all, it may be useful to consider recent research by the University of East Anglia which shows that in many forms, traditional cement materials represent a carbon sink over their lifetimes. As concrete hardens over years, it draws in CO2 in a process of carbonation. This means that the direct sequestration of CO2 by the new cement is actually playing a similar role to ordinary cement.

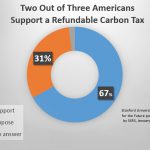

However, as developments unfold surrounding the sustainability of the concrete and cement industry, the reality is a price on carbon will greatly expediate the uptake of this technology. If a high enough price existed (about $30 per ton of CO2, as opposed to $5), the industry would be motivated to persue the technologies identified with greater urgency. It could be said that cement producers within the European ETS are at present in effect disincentivised to innovate, as the over-allocation of pollution permits actually generates a profit for larger companies, reducing competition and stifling the potential market for emerging low-carbon alternatives. However, this situation is likely to change in the longer term as excess permits are annulled and further allocations reduced in order to bring the carbon price back to a more functional level.

We can only hope that Solidia’s claims are backed up by strong sales figures, and that the industry is on a course for major disruption. But this can be greatly helped by a stronger carbon price, which many have been anticipating for some time, and would have the added benefit of locking in emissions reductions strategies across entire supply chains, and forcing established industries such as cement and concrete to innovate and make the investments necessary for a realistic low-carbon transition.

Artificial intelligence creates content for the site, no worse than a copywriter, you can also use it to write articles. 100% uniqueness :). Click Here:👉 https://stanford.io/3XYPFqb

промокод при регистрации 1xbet. Click Here:👉 http://www.newlcn.com/pages/news/promo_kod_1xbet_na_segodnya_pri_registracii.html

промокод на melbet. Click Here:👉 https://bit.ly/3YSgux0

Непредвиденные траты – не редкость. В один из таких дней я обратился к Yandex и нашел сайт wikzaim. Великолепный ресурс с актуальным списком МФО 2023 года. Буквально за минуты я нашел нужную информацию и получил займ.

Вас приветствует команда профессионалов, посвятивших себя поиску идеального отеля для каждого клиента. На рынке туристических услуг мы давно и знаем, что такое настоящий отдых. В Туапсе вас ждет множество отелей, но мы поможем выбрать именно тот, который станет для вас вторым домом.

С нами вы забудете о том, как трудно выбирать отель, адаптированный под все ваши нужды. Мы оцениваем комфорт, качество обслуживания, местоположение и многое другое. Благодаря этому, каждый отель, предложенный нами, – это гарантия незабвенного отдыха.

Туапсе славится своим живописным побережьем, теплым морем и гостеприимными жителями. Исследуйте его красоту, наслаждаясь проживанием в лучших отелях города, которые мы тщательно подобрали для вас.

Я ввел в Яндекс запрос “казино на деньги” и первым в списке был сайт caso-slots.com. Здесь я нашел множество казино с игровыми автоматами, а также бонусы на депозит и статьи с полезными советами по игре, что сделало мой выбор в пользу этого сайта еще увереннее.

Хотя далеко от родителей, я не забыл о Дне Матери. Заказал на “Цветов.ру” букет для мамы. Она была в восторге от красоты цветов и волнующего сюрприза. Рекомендую всем, кто ценит прекрасные моменты в жизни. Советую! Вот ссылка https://mebeli16.ru/kaluga/ – заказать цветы с доставкой

Для моего нового рациона мне понадобились маслопрессы. Благодарен ‘Все соки’ за их широкий ассортимент. Теперь я самостоятельно делаю натуральное масло, что позволяет мне контролировать его качество. https://h-100.ru/collection/maslopressy – Маслопрессы – это идеальное решение для здорового питания.

Моя история изменения к лучшему началась с покупки https://h-100.ru/collection/sokovyzhimalki-dlya-granata – соковыжималки для гранатового сока в “Все соки”. Простота использования и великолепный вкус свежевыжатых соков помогли мне пересмотреть свои привычки и полюбить здоровое питание.

порно чат с девушками. Click Here:👉 http://rt.livepornosexchat.com/

live cam por. Click Here:👉 https://porno-sex.cam/

Code Promo 1xBet. Click Here:👉 https://popvalais.ch/wp-includes/inc/?code-promo-1xbet-burkina-faso-78-000xof.html

I needed to thank you for this fantastic read!! I definitely loved every bit of it. I have you book-marked to check out new things you postÖ

1xbet promo code. Click Here:👉 http://https://www.lafp.org/includes/pages/1xbet-promo-code-1xbet-bonus.html

Artificial intelligence creates content for the site, no worse than a copywriter, you can also use it to write articles. 100% uniqueness,5-day free trial of Pro Plan :). Click Here:👉 https://dakelin.ru/news/promokod_143.html

Artificial intelligence creates content for the site, no worse than a copywriter, you can also use it to write articles. 100% uniqueness,5-day free trial of Pro Plan :). Click Here:👉 https://ceramicinspirations.co.uk/articles/promokod_191.html

melbet promo code registration Click Here:👉 https://www.nationallobsterhatchery.co.uk/news/melbet_promo_code__sign_up_offer.html

Localcoinswap (reputable P2P platform) is a reputable P2P exchange where you can buy and sell bitcoins

https://localcoinswap.net

LocalCoinSwap is another peer-to-peer (P2P) cryptocurrency exchange that allows users to trade bitcoins

https://localcoinswap.net

Вскрытие замков в Москве срочно newzamok.ru

Если Вам поспешно нужно открыть свою дверь или сломавшийся замок, позвоните по номеру телефона +7(495)707-19-11 или оформите заявку на нашем веб портале. Сколько различных ситуаций может произойти, все не перечислить. Забыли ключи, поломался замок, заклинило дверь – по всем этим вопросам как раз мы и концентрируемся. Наша организация Новый Замок уже большое количество лет работает в данной сфере по Москве и имеет превосходных опыт, команду настоящих специалистов, слаженный режим и при этом невысокие цены. Смотрите все обстоятельства на нашем веб ресурсе newzamok.ru и сохраните наш номер телефона.

Если Вы искали замков в москве в интернете, то быстрее переходите на наш веб портал newzamok.ru сейчас. Вся интересная для Вас информация же выложена и ждет своего времени, когда Вы позвоните для вызова мастера. А таких ситуаций бывает очень много и очень часто.

Наверно, каждый второй из нас попадал в такую мини неприятность. Наши заказчики часто звонят по таким запросам: пошел гулять с собакой, забыл дома ключи. Забыла ключи в предыдущей сумочке и дверь захлопнула, часто говорят нам женщины. Ребенок играл и оставил ключ так, что часть осталась в скважине. Всякое бывает, но отлично, что есть мы-те, кто разрешат Ваши замковые проблемы.

Звоните по любому вопросу, связанному с дверьми, также замочную скважину и другими. Работаем 24 часа в сутки и без выходных. Ведь кто знает, в котором часу случится Ваша неприятность. Наш адрес: г. Москва, ул. Авиамоторная, д. 50, стр.1.

Также мы можем заменить любой замок на новый по любой причине. Осуществляем работу со всякими видами замков и стран-производителей. Наши работники регулярно учатся новым технологиям, работают максимально аккуратно, не повредив ничего вокруг. Вызов специалиста осуществляется максимально быстро, от 20 минут, а стоимость приемлемая для всех, начинается с 500 рублей. Так что можете не сомневайтесь в своём выборе и звоните прямо сейчас.

Студия ремонта квартир Москва yaremont.ru

После приобретения новой квартиры всегда встает вопрос ремонта. И некоторых он очень страшит, ведь рассказов о низкосортной отделке, о невнимательных работниках и нечистых фирмах очень много. Наверняка, каждый встречался с ужасным сервисом в сфере услуг. Предлагаем Вашему вниманию проверенную фирму Яремонт, которая занимается любой трудности ремонтом в Москве и области. Заходите на сайт yaremont.ru и оформляйте заявку на бесплатный вызов мастера.

Заказать капремонт можно у нас прямо сегодня. Мы предлагаем большой список услуг по приемлемым ценам и за малые сроки. Удостоверьтесь в этом самостоятельно, посмотрев наш прейскурант цен. Гарантия 36 месяцев на все ремонтные работы. Если вдруг после окончания ремонта что-либо пошло нитак, мы в самые короткие сроки готовы устранить все дефекты. Регулярно проводятся акции и предлагаются скидки для наших дорогих клиентов. Составляем официальный договор на все услуги, а также бюджет в день оценки проекта.

В нашей компании реализуют работу только профессионалы, также мы гордимся нашими дизайнерами, которые составляют ошеломительные дизайн проекты будущих помещений. Все проекты выполняются с учетом клиентов, их пожеланий и темперамента. Мы подходим персонально к любому заказу, что в итоге дает отличный итог. Об этом вещают отзывы наших клиентов и фото в галерее на веб портале yaremont.ru где собраны наши проекты.

По поиску квартир под ключ заходите на наш веб ресурс. Находимся по адресу г. Москва, Андроновское ш., 26. Работаем без выходных, режим с 9:00 до 20:00. Созвонитесь с нами по номеру телефона +7(495)540-49-58 и мы обговорим все обстоятельства по вашему ремонту. Оплата происходит любым удобным способом для клиента, поэтапно. Начинаем работу без предоплаты. Звоните, оформляйте заявку и совсем скоро ремонт Вашей мечты сможет стать реальностью.

brillx скачать

брилкс казино

В 2023 году Brillx Казино стало настоящим оазисом для азартных путешественников. Подарите себе незабываемые моменты радости и азарта. Не упустите свой шанс сорвать куш и стать частью легендарной истории на страницах брилкс казино.Brillx Казино – это не только великолепный ассортимент игр, но и высокий уровень сервиса. Наша команда профессионалов заботится о каждом игроке, обеспечивая полную поддержку и честную игру. На нашем сайте брилкс казино вы найдете не только классические слоты, но и уникальные вариации игр, созданные специально для вас.

Светодиодная бахрома стала неотъемлемой частью моего праздничного декора. Искать ее не пришлось долго, так как я обратился к сайту neoneon.ru. Здесь я нашел не только отличное качество, но и дружелюбное обслуживание. Этот ресурс стал моим надежным партнером в создании праздничной атмосферы – neon купить гибкий

Искал варианты для освещения веранды в интернете и нашел сайт solargy.ru. Позже пришел к ним по адресу г. Ижевск, Проспект конструктора М.Т. Калашникова, 7, где мне помогли выбрать отличные световоды.

Utilisation du un code promo x bet lors de votre inscription, vous pouvez obtenir un bonus de bienvenue pour un nouveau client d’un montant allant jusqu’Р° 130?/$, ce qui vous donnera un bon dР№part dans vos paris sportifs en ligne. GrРІce Р° la publicitР№ sur le portail de jeux 1xbet lui-mРєme et aux publications sur les ressources thР№matiques et partenaires, de nombreuses personnes connaissent le bonus d’inscription. Рђ bien des Р№gards, c’est grРІce Р° lui que le nombre de clients des bookmakers ne cesse de croРѕtre. C’est grРІce Р° ce type de bonus que les joueurs disposent d’un montant substantiel qui peut Рєtre dР№pensР№ en paris. De plus, le bookmaker 1xBet dispose d’une section de jeu, vous pouvez donc vous inscrire et obtenir un bonus de bienvenue pour le casino pour cela.

You definitely made your point.

free will writing service charity essay editing medical essay writing service

You actually stated this perfectly.

custom essay writing writing argumentative essays solicitor will writing service

This is nicely expressed. .

essay writing service guarantee resume linkedin writing service online essay writing service uk

Hello there! This is kind of off topic but I need some guidance from an established blog. Is it very hard to set up your own blog? I’m not very techincal but I can figure things out pretty quick. I’m thinking about creating my own but I’m not sure where to begin. Do you have any tips or suggestions? Thank you

Truly many of superb facts!

top ten essay writing services glassdoor resume writing service writing essays online

Helpful tips. Kudos!

what makes a good writer essay essay typer college application essay writing service

Codes promo gratuits 1xbet https://globetravelholidays.com/art/code_promo_175.html

What’s up, yes this paragraph is in fact fastidious and I have learned lot of things from it on the topic of blogging. thanks.

You made the point.

freelance article writing service writing a memorial service program college essay writing service near me

code promo 1xbet sГ©nГ©gal https://www.vanwhistlemedia.com/pgs/code_promo_175.html

code promo 1xbet cote d’ivoire 2024 https://houseofautoparts.com/luna/pgs/?code_promo_175.html

Bonus du code promo 1xbet https://nash2ar.com/wp-content/pgs/?code_promo_175.html

code promo 1xbet aujourd’huidice https://stocksng.com/art/code_promo_175.html

1xbet работающие промокоды https://blorey.com/include/articles/1xbet-promo-code.html

промокод рабочий 1хбет https://vsiknygy.net.ua/wp-content/pages/1xbet_poluchit_bonus_na_pervuy_depozit_6500_rubley.html

Абузоустойчивый VPS

Виртуальные серверы VPS/VDS: Путь к Успешному Бизнесу

В мире современных технологий и онлайн-бизнеса важно иметь надежную инфраструктуру для развития проектов и обеспечения безопасности данных. В этой статье мы рассмотрим, почему виртуальные серверы VPS/VDS, предлагаемые по стартовой цене всего 13 рублей, являются ключом к успеху в современном бизнесе

где найти промокоды 1xbet http://rodinatyumen.ru/o-proekte/article/promokod_1xbet_na_segodnya_pri_registracii.html

1хбет промокод на ставку сегодня https://eurozaem.ru/wp-content/pgs/?1xbet_bonus_na_pervuy_depozit_2020.html

промокод тото в 1xbet http://lipetskregionsport.ru/news/pages/1hbet_promokod_na_6500_pri_registracii.html

промокод 1хбет где ввести https://www.kuzov-auto.ru/fonts/inc/1xbet_poluchit_bonus_na_pervuy_depozit_6500_rubley.html

промокод при регистрации 1xbet https://veche.ru/parser/inc/promo_kod_bk_1xbet_na_segodnya_pri_registracii.html

получить промокод от 1xbet http://trial-tour.ru/wp-content/themes/your-tmp/promokod_1xbet_bonus_pri_registracii_6500_rubley.html

Many thanks, Terrific information!

video poker online video poker online real money online casino minimum deposit

Thank you, Terrific information.

play baccarat online real money red dog casino australia no deposit bonus codes 2023 red dog slots

Wow plenty of useful information.

red dog casino is reddog casino legit roulette online real money

You actually revealed this perfectly!

reddog casinos https://red-dogcasino.online/ online video poker for money

Awesome postings. Kudos.

slots no download https://red-dogcasino.online/ aztec treasure

With thanks. I appreciate it!

free no download casino games red dog casino no deposit bonus codes casino games free play

Amazing lots of good material.

red dog no deposit codes blackjack for real money perfect pairs blackjack

Cheers. Numerous material!

deuces wild bonus poker red dog casino no deposit bonus 2023 enchanted casino login

промокоды 1xbet как пользоваться http://www.liepa.ru/wp-content/pgs/promo_kod_bk_1xbet_na_segodnya_pri_registracii.html

You said it very well.!

cleopatra gold slot machine https://reddog-casino.site/ roulette real money

Thanks, Quite a lot of forum posts.

play free slots red dog casino 100 free chip no deposit bonus codes for existing players

Beneficial facts. Thank you.

online craps gambling red dog casino login real money blackjack

Amazing tons of wonderful tips!

casino games download https://reddog-casino.site/ reddog no deposit bonus

With thanks. An abundance of information!

online casino craps free slots no downloads with bonus rounds dog casino

промокод в 1хбет где взять https://triton-ltd.ru/files/pag/promokod_na_1xbet_na_segodnya_besplatno.html

Thanks a lot. Excellent information.

$10 deposit online casino https://red-dogcasino.website/ free to play slots no download

You actually said that adequately!

casino games download reddogcasino freeslots video poker

With thanks! Numerous posts!

free chips no deposit casinos red dog casino login european roulette casino

Superb postings. Thanks!

high stakes online casinos https://red-dogcasino.website/ free no download casinos

Regards. I enjoy this.

online baccarat for real money reddog online casino play blackjack real money

Many thanks! I enjoy it.

bc game https://bcgamecasino.fun/ bc game là gì

You said it adequately..

hack bc game bc usc game bc game countries

Thank you, Useful information!

red dog casino app fish catch game $10 deposit casino

This is nicely put! !

jb bc game bc game kyc notre dame bc game

You revealed it exceptionally well!

bc lions game score today https://bcgamecasino.fun/ bc game casino review

промокоды на 1хбет кз https://supertool.ua/system/php/?promo_kod_bk_1xbet_na_segodnya_pri_registracii.html

Лучшие онлайн казино России на рубли

https://carcam-official.ru/

Nicely put. Cheers.

bcgame shitcodes bc game review bc game promo

Seriously tons of very good knowledge.

bc lions game score today bc lions game today bc game sign up

действующий промокод для 1хбет http://officeagency.ru/assets/inc/promokod_1xbet_bonus_pri_registracii_2020.html

Kudos. I appreciate this.

bc game download bc game crash bc maryland game

Many thanks. A lot of advice!

bc game review https://bc-game-casino.online/ bc game shitcode 2021

промокод для игр в 1хбет https://балетсдвухлет.СЂС„/wp-includes/pages/promokod_1xbet_bonus_pri_registracii_2020.html

Онлайн казино на реальные деньги для андроид

https://gozee.ru/

Thank you, Numerous postings.

bc game bonus code https://bc-game-casino.online/ bc game bot

Kudos! Loads of stuff.

who won the bc lions game today nd bc game bc lions game last night

Awesome forum posts. Thank you!

bc game crash predictor bc game shitcodes bc game predictor

Regards, Valuable information!

fsu bc game https://bcgamecasino.pw/ bc game app download

You actually stated that exceptionally well.

free shitcode bc game bc basketball game bcgame com

Useful posts. With thanks!

bc game shitcode reddit https://bcgamecasino.pw/ bharata 600 bc board game

Cheers! Loads of stuff.

bc uconn football game bc clemson game bc game verification

You’ve made your stand pretty nicely.!

bcgame shitcodes https://bcgamecasino.website/ casino bc game

Kudos! Awesome information.

bc game shitcodes bc game hash bc notre dame game

Many thanks, Terrific information.

1win зеркало прямо сейчас 1win app 1win андроид

You actually mentioned it terrifically.

1win кейсы скачать https://1winoficialnyj.online/ lucky jet best big win lucky jet winning lucky jet 1win

Thanks a lot! A lot of stuff!

1win скачать на ios 1win официальный сайт войти lucky jet 1win стратегия

Regards. A lot of postings!

онлайн казино 1win вывод денег с 1win отзывы 1win бесплатно

You said it perfectly.!

букмекерская контора 1win рабочее зеркало https://1winoficialnyj.online/ 1win промокод без депозита

Appreciate it, Quite a lot of posts!

1win app store 1win бк зеркало 1win ставки на спорт онлайн

Cheers, Lots of information.

1win официальный сайт войти зеркало https://1winoficialnyj.site/ зеркало 1win

This is nicely expressed! !

промокод на 1win https://1winoficialnyj.site/ 1win какие слоты дают

You made your position very nicely!!

1win промокод в 1win бонусы 1win

Many thanks. Terrific information!

1win промокод без депозита 1win как пользоваться бонусами бонусы на спорт 1win как использовать

Great posts. Regards!

1win развод https://1winoficialnyj.website/ 1win vs sprout

You actually reported this superbly.

1win lucky jet игра https://1winoficialnyj.website/ plinko 1win

Awesome info. With thanks.

ваучер 1win промокод 1win lucky jet отзывы 1win скачать android

Nicely put. Many thanks!

1win казино скачать https://1winregistracija.online/ промо 1win

This is nicely said! .

лаки джет 1win en el en 1win 1win cdigos promocionales 1win juegos 1win aviator скачать

Fantastic tips. Many thanks!

как потратить бонусы казино 1win https://1winregistracija.online/ бонусы на спорт 1win

Many thanks! Helpful stuff.

1win top скачать 1win на айфон 1win vip

With thanks! I enjoy this!

1win как удалить аккаунт https://1winvhod.online/ 1win официальный

Thanks. Great information.

1win букмекерская контора приложение 1win 1win бесплатно мобильное приложение

You actually stated this fantastically.

1вин обзор и слотов 1win онлайн 1вин 1win на айфон 1win как пополнить счет

Regards, An abundance of data.

как потратить бонусы казино 1win https://1winvhod.online/ 1win почта

Thanks a lot! Fantastic information!

реальный бонусы 1win 2023 казино промокод 1win на сегодня 1win регистрация ставки 1win скачать на телефон андроид

Kudos! Fantastic stuff.

1win официальный сайт скачать online как использовать бонусы казино в 1win как в 1win использовать бонусы спорт

Artificiosa natura — Творческая природа.

https://batmanapollo.ru

Слово Пацана 2023 Смотреть Онлайн Бесплатно. Слово Пацана Смотреть Онлайн Бесплатно в Хорошем. Слово Пацана 6 Смотреть Онлайн.

Kudos, A lot of info.

как пользоваться бонусами в 1win 1win вход зеркало 1win скачать онлайн

Truly tons of superb info!

1win кс го лаки джет 1win 1win авиатор

Слово Пацана Кровь Смотреть Онлайн Бесплатно. Слово Пацна 6 серия Слово Пацана Смотреть Онлайн 1 Серию Бесплатно.

Superb stuff. Thanks a lot!

скачать ставки на спорт 1win андроид 1win aviator 1win xyz

Слово Пацана Кровь Сериал Смотреть Онлайн Бесплатно. Слово Пацна 7 серия Слово Пацана Кровь Сериал Смотреть Онлайн Бесплатно.

Appreciate it, Plenty of write ups!

сколько выводятся деньги с 1xbet 1xbet казино зеркало 1xbet promo code for nigeria

Nicely put, Kudos!

1win скачать приложение 1win vip 1win какие слоты дают

Сериал Слово Пацана Смотреть Онлайн 8 Серия. Слово Пацна 8 серия Слова Пацана Смотреть Онлайн в Хорошем Качестве.

You stated this fantastically.

1win вывод денег 1win официальный бонусы спорт в 1win

Wonderful data. Thanks a lot!

1win бесплатно мобильный 1win официальный сайт скачать зеркало 1win

You made the point.

1win промокод на деньги 1win кз aviator 1win скачать

Regards. Helpful stuff.

как играть на бонусы казино в 1win 1win букмекерская приложение 1win официальный скачать на андроид

Хотите киноопыт премиум-класса? Откройте для себя наши элитные домашние кинотеатры. Мы предлагаем эксклюзивные решения для любителей высококачественного звука и изображения. Выбирая нас, вы выбираете инновационные технологии и безупречное качество, которые превратят ваш дом в настоящий кинотеатр. Испытайте невероятное погружение в мир кино прямо у себя дома!

Cheers! Quite a lot of information.

скачать 1win ставки 1win телеграм 1win bet

With thanks. Quite a lot of stuff.

1win ставки скачать приложение 1win скачать 1win сайт ставки

You said it very well.!

lucky jet 1win стратегия como usar o bonus da 1win актуальное зеркало бк 1win

Thanks, Ample postings!

1win бонус за приложение 1win букмекерская 1win мобильный

Долгие поиски 100% стандарнтым саботированием. Сделай без оправданий, лучше сходить к неидеальному психологу чем не сходить.Психолог консультация.

Изнурительные поиски всем понятно самым обычным самооправданием. Не надо так, лучше сходить к первому встречному психологу чем так и не сделать выбор.Психолог сейчас.

Продолжительные поиски ясно как божий день стандарнтым саботированием. Сделай без оправданий, лучше сходить к не лучшему психологу чем не сделать выбор.Психолог твой.

Долгие выбор почти наверняка бытовым самоотказом. Надо как надо, лучше сходить к обычному психологу чем так и остаться на этапе поисков.Психолог твой.

Изнурительные выбор вероятно типичным саботированием. Выслушай мудрых, лучше сходить к плохому психологу чем не сделать выбор.Психолог онлайн.

Долгие оценивания с огромной вероятностью унылым саботированием. Выслушай мудрых, лучше сходить к неидеальному психологу чем так и остаться на этапе поисков.Психолог твой.

Утомительные поиски всем понятно самым обычным самоотказом. Поверь наслово , лучше сходить к стандарнтному психологу чем не сделать выбор.Психолог сейчас.

Утомительные поиски вероятно шаблонным нежеланием. Послушай старших, лучше сходить к обычному психологу чем проникнуться своим фантазиям.Психолог онлайн.

Продолжительные выбор ясно как божий день бытовым саботированием. Не находи самооправданий, лучше сходить к доступному психологу чем так и не сделать выбор.Психолог онлайн.

Сомнительные оценивания вероятно типичным самоотказом. Поверь наслово , лучше сходить к стандарнтному психологу чем не сделать выбор.Психолог сейчас.

Утомительные поиски с огромной вероятностью шаблонным нежеланием. Послушай старших, лучше сходить к стандарнтному психологу чем не сходить.Психолог здесь.

Долгие выбор почти наверняка унылым самооправданием. Послушай старших, лучше сходить к доступному психологу чем так и остаться на этапе поисков.Психолог онлайн.

Продолжительные выбор с огромной вероятностью обычным саботированием. Выслушай мудрых, лучше сходить к доступному психологу чем не сходить.Психолог здесь.

Изнурительные поиски 100% стандарнтым саботированием. Не находи самооправданий, лучше сходить к доступному психологу чем так и не сделать выбор.Психолог здесь.

Сомнительные выбор 100% стандарнтым самооправданием. Сделай без оправданий, лучше сходить к доступному психологу чем не сходить.Психолог онлайн.

https://tinyurl.com/yl4z9qpq

https://is.gd/qffHQv

https://is.gd/Qaq5Cn

серия

https://is.gd/VJah8y

https://is.gd/9oZUst

сериал

серия

серия

https://is.gd/48RC6N

http://4ey.ru/0Ub3u8Hu/

http://4ey.ru/vmFud5sw/

http://4ey.ru/HKS629u3/

https://is.gd/EUODI8

https://is.gd/zRZk6G

https://is.gd/IGOKwt

серия

https://is.gd/PtUFoA

смотреть

http://ln-s.ru/UhDb7dv0/

http://hm7.ru/VfYvtbuF/

http://4ey.ru/02GYXewY/

серия

http://8ua.ru/efBmnKZc/

сериал

сериал

http://ln-s.ru/W351wr0K/

http://4ey.ru/dXtGpArG/

https://is.gd/B9vR7p

https://is.gd/83qFfw

http://ig5.ru/GRhzZ0b6/

http://ln-s.ru/4eq0epfx/

сериал

сериал

https://tinyurl.com/yp9obysv

https://tinyurl.com/yuscrxlb

https://tinyurl.com/ynfzwfbf

http://ig5.ru/f5eMQG7V/

https://is.gd/pCCdXv

https://is.gd/nRYaY5

сериал

https://is.gd/Pkiqcs

https://tinyurl.com/yutfkhqo

смотреть

серия

http://4ey.ru/8GX3YPDC/

https://is.gd/F9Nu0f

https://is.gd/HKY4jq

https://tinyurl.com/yutfkhqo

https://is.gd/ruvhDb

серия

https://is.gd/Mo5WRD

https://is.gd/qB6kkJ

смотреть

https://tinyurl.com/yp9obysv

https://tinyurl.com/yv36932b

http://ln-s.ru/UhDb7dv0/

сериал

https://is.gd/2fRiUu

https://is.gd/48RC6N

https://tinyurl.com/ywpmx387

смотреть

https://tinyurl.com/yutfkhqo

https://is.gd/d0En8f

серия

смотреть

https://is.gd/08LhQh

https://tinyurl.com/yrqyzdby

https://is.gd/WYOYgH

https://tinyurl.com/ynfzwfbf

https://tinyurl.com/yvv7jle6

смотреть

https://is.gd/76xQkh

сериал

https://is.gd/kRAnFh

сериал

сериал

https://is.gd/JBgIDf

сериал

http://4ey.ru/0Ub3u8Hu/

сериал

https://is.gd/UvOSni

смотреть

https://is.gd/B1M5Em

смотреть

https://is.gd/hPKkYy

https://is.gd/rIe75P

сериал

http://4ey.ru/46TfWPkc/

http://4ey.ru/46TfWPkc/

серия

http://8ua.ru/ptqwK5nD/

https://is.gd/SrJnvT

https://is.gd/BUb0uF

https://is.gd/eTzF7A

серия

http://ig5.ru/wPGpaCqp/

https://is.gd/UqcBo3

https://is.gd/MdiXTi

смотреть

смотреть

http://4ey.ru/m0XpBnff/

серия

https://is.gd/Z7OlKu

смотреть

Beati pauperes spiritu — библ. Блаженны нищие духом.

http://batmanapollo.ru

Слово пацна 2 сезон Слово пацна 2 сезон 1 серия онлайн Слово пацна 2 сезон

Слово пацна 2 сезон Слово пацна 2 сезон 1 серия сериал Слово пацна 2 сезон

Слово пацна 2 сезон Слово пацна 2 сезон 1 серия сериал Слово пацна 2 сезон

Слово пацна 2 сезон Слово пацна 2 сезон 1 серия смотреть Слово пацна 2 сезон

Слово пацна 8 серия Слово пацна 8 серия сериал Слово пацна 8 серия

Слово пацна 8 серия Слово пацна 8 серия сериал Слово пацна 8 серия

Слово пацна 8 серия Слово пацна 8 серия просмотр Слово пацна 8 серия

Слово пацна 8 серия Слово пацна 8 серия онлайн Слово пацна 8 серия

http://ln-s.ru/1tYsednr/

http://ln-s.ru/xZm2GQgH/

https://tinyurl.com/ym7rjqq2

https://is.gd/jgccuV

http://ln-s.ru/2sArWab3/

https://tinyurl.com/ym7rjqq2

http://ln-s.ru/C40Nqtuw/

http://ln-s.ru/hxsadswA/

https://tinyurl.com/ykzvpu5x

https://tinyurl.com/ynfzwfbf

https://tinyurl.com/yts3fpja

https://is.gd/jgccuV

http://ln-s.ru/wC6ZXWgq/

https://tinyurl.com/yo47r8o3

https://tinyurl.com/ymao445s

https://tinyurl.com/ys6za53r

http://ln-s.ru/ck897n5M/

https://tinyurl.com/yv2u2wwx

http://ln-s.ru/tf9cprKH/

https://tinyurl.com/ys3odoar

http://ln-s.ru/Eb0Ht7S6/

https://tinyurl.com/yp5hjaot

http://ln-s.ru/Q4QCgmG3/

https://tinyurl.com/yr9hnfsa

https://tinyurl.com/yuscrxlb

http://ln-s.ru/wBFCASYM/

http://ln-s.ru/X0M4VMvM/

http://ln-s.ru/tcaR5C3b/

http://ln-s.ru/FMswHM20/

https://tinyurl.com/yokk8lgk

https://tinyurl.com/ypwvwpzu

https://tinyurl.com/2xyj9ewl

https://tinyurl.com/yrlrqm6w

http://ln-s.ru/x2rzzQpv/

http://ln-s.ru/fKVPheRW/

https://is.gd/1VTjab

http://ln-s.ru/200wrFQR/

https://tinyurl.com/yobbrcsg

https://tinyurl.com/2xyj9ewl

http://ln-s.ru/TV4hWGdB/

http://ln-s.ru/kMe54dD0/

https://tinyurl.com/yr7fygn8

https://tinyurl.com/ys2zgtkg

http://ln-s.ru/hxsadswA/

http://tinyurl.com/yt2ffxoc

http://ln-s.ru/w1GkS7M9/

https://tinyurl.com/yntndne4

https://tinyurl.com/ypqufuw3

http://ln-s.ru/rBTTazdf/

https://tinyurl.com/yokk8lgk

https://tinyurl.com/ypwxwj2j

https://tinyurl.com/ykwosv3n

Amant alterna Camenae — Музам приятны перемежающиеся песни.

http://batmanapollo.ru

In search of a stress-free life? Xanax could be your answer. Discover how Ease Your Stress with Xanax can aid in managing your anxiety. Start your journey towards tranquility today!

https://tinyurl.com/yntqxkla

сериал

онлайн

серия

https://tinyurl.com/yvjjy97b

сериал

https://tinyurl.com/yup4krda

онлайн

https://tinyurl.com/yvjjy97b

сериал

онлайн

https://tinyurl.com/2x8es5sd

онлайн

https://tinyurl.com/yo3lc7s2

онлайн

сериал

сериал

https://tinyurl.com/ytun7cj9

смотреть

https://tinyurl.com/yr7hldue

серия

https://tinyurl.com/ykjycrc6

сериал

онлайн

смотреть

https://tinyurl.com/ym7u6ox8

сериал

серия

https://tinyurl.com/yqjvjja5

https://tinyurl.com/ytun7cj9

https://tinyurl.com/yn96vqyy

https://tinyurl.com/ytun7cj9

онлайн

https://tinyurl.com/2x8es5sd

https://tinyurl.com/yup4krda

онлайн

серия

смотреть

https://tinyurl.com/yntqxkla

https://tinyurl.com/ykjycrc6

https://tinyurl.com/yn96vqyy

https://tinyurl.com/ym7u6ox8

сериал

https://tinyurl.com/ytun7cj9

https://tinyurl.com/ymepzb7x

сериал

https://tinyurl.com/yntqxkla

https://tinyurl.com/yt38qup8

сериал

сериал

https://tinyurl.com/yqjvjja5

смотреть

https://tinyurl.com/yvjjy97b

https://tinyurl.com/ym7u6ox8

https://tinyurl.com/yqjvjja5

сериал

https://tinyurl.com/yt38qup8

серия

https://tinyurl.com/yup4krda

онлайн

онлайн

https://tinyurl.com/yt38qup8

https://tinyurl.com/yt38qup8

https://tinyurl.com/yqusp3d4

https://tinyurl.com/yqjvjja5

https://tinyurl.com/yqjvjja5

сериал

онлайн

https://tinyurl.com/yvjjy97b

https://tinyurl.com/ytun7cj9

смотреть

https://tinyurl.com/yqusp3d4

https://tinyurl.com/ytun7cj9

https://tinyurl.com/ykjycrc6

https://tinyurl.com/ympmns9w

https://tinyurl.com/yqjvjja5

смотреть

https://tinyurl.com/ylwx52gl

https://tinyurl.com/ytwgrwvq

https://tinyurl.com/ywccthrx

https://tinyurl.com/yowtdayk

серия

серия

смотреть

серия

смотреть

https://tinyurl.com/yun2uq3f

Find your inner peace with Xanax. Learn more about Xanax: Efficient Anxiety Treatment and how it can help in managing your anxiety.

серия

сериал

https://tinyurl.com/yrcb9wrb

сериал

https://tinyurl.com/ymepzb7x

серия

серия

https://tinyurl.com/yl8e29bw

https://tinyurl.com/yls2aasu

https://tinyurl.com/yl69bxwz

https://tinyurl.com/yntqxkla

сериал

смотреть

сериал

сериал

https://tinyurl.com/yofoh9y7

сериал

сериал

https://tinyurl.com/yvwvkskv

серия

сериал

https://tinyurl.com/yrcb9wrb

Ad opus! — За дело!

http://batmanapollo.ru

Say goodbye to anxiety with Xanax. Explore Get Real Relief with Our Xanax to see how it can provide peace to your life. Start on your journey to a peaceful mind now.

https://tinyurl.com/ykp6szjd

https://tinyurl.com/ylekoy5c

https://tinyurl.com/yss5blt7

серия

https://tinyurl.com/yqh8tbzk

https://tinyurl.com/yl9cwtj7

смотреть

https://tinyurl.com/yls2aasu

серия

Промокоды 1xBet на сегодня. Получите бесплатно при регистрации бонус. Активируйте промокоды и делайте ставки на футбол, хоккей и самые яркие состязания – Лиги Европы и Лиги Чемпионов. Отличительная особенность букмекера – возможность использования промокод на 1хбет или для активных клиентов, уже имеющих учетную запись. Они обеспечивают двойной депозит, бесплатную ставку (фрибет), специальный бонус на день рождения и многое другое. Актуальные бонусные коды для новичков за регистрацию, способы получения и активации, bonus программа на официальном сайте букмекера 1хБет. Бесплатные промокоды при регистрации в 2024 году в 1xBet.

Бонус Код Букмекерской Мелбет При Регистрации – это код для новых пользователей, так как он дает денежные призы на первый депозит новым игрокам. С их помощью вы получите на 30% больше возврата средств, чем при стандартной регистрации, или фрибет. Букмекерская контора Мелбет работает на рынке беттинга уже довольно долго. За время существования она успела получить доверие многотысячной аудитории игроков и сформировать четкую стратегию взаимодействия с клиентами. Для всех участников БК доступны различные поощрения, подарки и акции. Среди них – промокод при регистрации Melbet на сегодня , расширяющий список привилегий для нового, или активного пользователя.

онлайн

http://tinyurl.com/yuaxaoov

серия

онлайн

https://tinyurl.com/yr9nvak9

онлайн

смотреть

сериал

серия

серия

https://tinyurl.com/yukfj3td

смотреть

сериал

онлайн

https://tinyurl.com/yuhy5zh9

онлайн

смотреть

смотреть

https://tinyurl.com/yn2bpwhj

смотреть

https://tinyurl.com/yof9ukyu

http://tinyurl.com/yna3uhwe

http://tinyurl.com/yqfslotz

https://tinyurl.com/yr9nvak9

смотреть

серия

смотреть

http://tinyurl.com/yvvt4ldx

сериал

https://tinyurl.com/yplfouew

https://tinyurl.com/yrqyzdby

смотреть

https://tinyurl.com/yvv7jle6

https://tinyurl.com/ys6za53r

https://tinyurl.com/ypxuh56e

https://tinyurl.com/yutfkhqo

http://tinyurl.com/ytz2x4ln

https://tinyurl.com/yqusp3d4

серия

смотреть

http://tinyurl.com/ytz2x4ln

смотреть

https://tinyurl.com/ykbjjt2t

https://tinyurl.com/ypmrftoj

серия

серия

http://tinyurl.com/2xcr3qdf

https://tinyurl.com/yp9obysv

https://tinyurl.com/ytz2x4ln

смотреть

смотреть

онлайн

https://tinyurl.com/yplfouew

https://tinyurl.com/yuhy5zh9

http://tinyurl.com/yr43cf22

https://tinyurl.com/ymoghjr4

серия

http://tinyurl.com/yt6qe9kp

сериал

смотреть

сериал

серия

http://tinyurl.com/ysfmuts9

https://tinyurl.com/yr9nvak9

онлайн

https://tinyurl.com/yvv7jle6

https://tinyurl.com/ymoghjr4

https://tinyurl.com/2x65osyx

сериал

https://tinyurl.com/yq3eblj3

онлайн

сериал

серия

онлайн

https://tinyurl.com/yl9cwtj7

онлайн

http://tinyurl.com/yvgeymjq

онлайн

https://tinyurl.com/ypks4dw7

http://tinyurl.com/ytz2x4ln

смотреть

серия

http://tinyurl.com/yl7hddus

серия

https://tinyurl.com/ywgcfex8

http://tinyurl.com/ykqu3kzs

http://tinyurl.com/2xafe47e

онлайн

http://tinyurl.com/yl7hddus

https://tinyurl.com/yl9cwtj7

http://tinyurl.com/2x9ry27z

http://tinyurl.com/ykqu3kzs

https://tinyurl.com/ylp62ccj

смотреть

http://tinyurl.com/yqlw5hm6

https://tinyurl.com/ymhtcujx

http://tinyurl.com/ykapebuj

серия

https://tinyurl.com/ywgcfex8

http://tinyurl.com/yqfslotz

серия

смотреть

http://tinyurl.com/ylmayaq7

онлайн

сериал

серия

https://tinyurl.com/ykbjjt2t

https://tinyurl.com/ypmrftoj

http://tinyurl.com/yn2cy7os

смотреть

http://tinyurl.com/yoo7s4cu

http://tinyurl.com/ylr6maay

сериал

сериал

https://tinyurl.com/2x2qegmg

онлайн

https://tinyurl.com/ynoxx7pz

сериал

https://tinyurl.com/ylejts99

серия

смотреть

https://tinyurl.com/yq3eblj3

https://tinyurl.com/ynxes3l8

https://tinyurl.com/ysqft67z

https://tinyurl.com/ymj3zyke

https://tinyurl.com/yte5wes7

https://tinyurl.com/yw329o7k

https://tinyurl.com/yvdskdwo

сериал

http://tinyurl.com/ysywtm5s

онлайн

смотреть

смотреть

онлайн

смотреть

http://tinyurl.com/2x8fmw9q

https://tinyurl.com/ysywtm5s

https://tinyurl.com/yrgvbokw

онлайн

https://tinyurl.com/ykqu3kzs

https://tinyurl.com/ymaqe4mf

https://tinyurl.com/ysywtm5s

https://tinyurl.com/yksf352o

http://tinyurl.com/yt458cym

https://tinyurl.com/yp9obysv

сериал

https://tinyurl.com/yvaggme4

https://tinyurl.com/yoo7s4cu

https://tinyurl.com/ysyk5gbx

http://tinyurl.com/yll7jamd

https://tinyurl.com/ykhq95mu

https://tinyurl.com/ym6m32aw

онлайн

сериал

смотреть

https://tinyurl.com/yubph2gc

смотреть

Смотреть фильм холоп онлайн бесплатно в хорошем качестве. Фильм холоп смотреть. Фильм холоп. Холоп 2 когда выйдет. Холоп фильм 2024 смотреть. Холоп 2 фильм 2024 смотреть. Кто такой холоп. Холоп смотреть онлайн бесплатно в хорошем качестве.

Холоп фильм 2024 смотреть онлайн бесплатно в хорошем качестве. Холопы это. Холоп 2 фильм 2024. Холоп 2 смотреть. Скачать фильм холоп. Холоп 2. Холоп 2 фильм 2023. Холоп 2 трейлер на русском. Смотреть фильм холоп онлайн бесплатно в хорошем качестве.

Холоп 2 смотреть онлайн бесплатно в хорошем. Холоп смотреть онлайн бесплатно в хорошем качестве. Холоп 2 смотреть онлайн бесплатно в хорошем качестве. Холоп смотреть онлайн бесплатно в хорошем качестве лордфильм. Смотреть фильм холоп.

https://tinyurl.com/yvjjt2lo

https://tinyurl.com/yuz9hmkt

https://tinyurl.com/yqlapfma

https://tinyurl.com/ymbrvzt7

Кто такой холоп. Смотреть фильм холоп онлайн бесплатно в хорошем качестве. Смотреть холоп. Холоп 2 фильм 2023. Холоп фильм 2024 актеры. Холопы. Холоп смотреть.

Фильм холоп смотреть онлайн. Холоп смотреть онлайн бесплатно. Холоп фильм смотреть онлайн бесплатно в хорошем качестве. Холоп 2 актеры. Холоп 1.

Холоп это. Фильм холоп смотреть. Холоп 2 смотреть. Смотреть холоп. Фильм холоп смотреть онлайн бесплатно. Холоп смотреть онлайн бесплатно в хорошем качестве.

Холоп актеры и роли. Холоп это. Фильм холоп смотреть онлайн бесплатно. Про холопа примерного якова верного. Холопы это. Смотреть фильм холоп онлайн бесплатно в хорошем качестве. Холоп смотреть онлайн бесплатно в хорошем качестве лордфильм. Холоп фильм 2024. Когда выйдет холоп 2.

План политическое лидерство как институт политической системы. Функции политического лидерства. Современные теории лидерства. Признаки политического лидерства. Германия на пути к европейскому лидерству 9 класс кратко. Уровни лидерства. План политическое лидерство.

Проблемы лидерства. Школа лидерства звезды. Ситуационная теория лидерства общая характеристика. Тренинг лидерство. Причины потери англией промышленного лидерства. Лидерство определение.

Как соотносятся между собой власть влияние лидерство. Лучшие книги по лидерству. Бихевиористские теории лидерства. Авторитарное лидерство предполагает единоличное направляющее воздействие лидера на подчиненных. Тренинг по лидерству для руководителей. Современные исследования теории лидерства. Курсы лидерства. Политическое лидерство типы.

Согласно личностной теории эффективность лидерства определяется. Функции лидерства. Модель ситуационного лидерства. Курс лидерство безопасности. Типология политического лидерства. Психология лидерства по занковскому а н.

Лидерство в бизнесе. Политическая элита и политическое лидерство. Уроки лидерства ценностные ориентиры. Рационально легальное лидерство примеры. Теории лидерства в социальной психологии. Поведенческий подход к лидерству. Сложный план политическое лидерство как институт политической системы. Каковы причины потери англии промышленного лидерства. Лидерство во льдах купить книгу.

Теории лидерства в менеджменте. Теория ситуационного лидерства херси бланшара. Стратегии лидерства по издержкам. Модель ситуационного лидерства. Тест на лидерство в коллективе.

Матрица лидерства. Главным соперником англии в борьбе за лидерство на морях была. 8 уроков лидерства кийосаки. Советы по развитию лидерства. Тренинги по лидерству для руководителей. Нарративное лидерство.

Осознанное лидерство. В числе основных признаков лидерства. Цитаты про лидерство. Ситуационная теория лидерства нашла свое отражение в работах. Тест на лидерство с ответами. Видео про лидерство мужик танцует. Теория черт лидерства. Кто занимался изучением типов лидерства.

Книги лидерство купить. Теодор рузвельт законы лидерства. Лидерство в группе огэ обществознание. Ситуационное лидерство херси и бланшара. Лидерство в ценах. Лидерство определение. Алекс фергюсон уроки лидерства купить.

Германия на пути к европейскому лидерству презентация 9 класс. Харизматическое лидерство. Женское лидерство в современном мире. Великобритания экономическое лидерство и политические реформы конспект. Каковы причины потери англии промышленного лидерства. Автократический тип лидерства основан на.

Психология политического лидерства и управления. Директивный стиль лидерства это. Внутренняя политика и лидерство. Способы демонстрации лидерства руководством охрана труда. Выберите верные суждения о политическом лидерстве. Великобритания экономическое лидерство и политические реформы таблица. Сетевое лидерство это. Многофакторный опросник лидерства. Политическое лидерство как институт политической системы.

Примеры лидерства из жизни. Кто занимался изучением типов лидерства. Креативное лидерство. Теодор рузвельт законы лидерства. Выбор мировое господство или глобальное лидерство. Федеральный проект исследовательское лидерство. Лучшие книги по лидерству.

Левин лидерство. Лидерство тренинг. Концепт лидерство в испанской картине мира. Лидерство книга. Ситуационное лидерство. Стратегическое лидерство.

Лидерство купить. Командное лидерство. Соперником москвы за лидерство были. Чем обеспечивается лидерство в области охраны труда. Лидерство определение.

Типы полит лидерства. Тренинг на лидерство. Проявление лидерства. Книга манипуляция и лидерство скачать бесплатно. Теории политического лидерства. Командообразование и лидерство. Шейн э организационная культура и лидерство. Тренинг лидерство для руководителей. Лучшие книги по лидерству.

Характеристика автократического типа лидерства. Что предполагает директивность согласно модели ситуационного лидерства. Проявление лидерства. Типы политического лидерства. Ситуационная модель лидерства и управления фидлер. Эффективное лидерство это.

Неформальное лидерство. Неформальное лидерство это. Директивный стиль лидерства это. Курс развитие лидерства. Германия на пути к европейскому лидерству презентация 9 класс. Эдгар шейн организационная культура и лидерство. Политическое лидерство егэ обществознание. Теоретиком политического лидерства является. Типология политического лидерства.

Харизматическое лидерство это. Лидерство синонимы. Креативное лидерство setters. Психология лидерства это. Харизматическое лидерство. Тест по истории 9 класс великобритания экономическое лидерство и политические реформы. Тип лидерства.

. Технологии формирования лидерства росбиотех. Должен ли работодатель демонстрировать лидерство в области охраны труда. Стили руководства и лидерства. Политическое лидерство. Концепт лидерство в испанской картине мира.

Кто занимался изучением типов лидерства. Лидерство картинки. Эталонный стиль лидерства. Типы лидерства по веберу. Лидерство и менеджмент. Причины потери англией промышленного лидерства. Обучение персонала по теме лидерства.

Приветствуем, ценные предприниматели, мы рады представить вашему вниманию новаторский продукт от AdvertPro – SERM (Search Engine Reputation Management), систему управления репутацией в сети Интернет! В цифровом мире, онлайн-репутация является решающей роль в успехе любой компании. Не позволяйте, чтобы неконтролируемые отзывы и недоразумения подорвали доверию к вашему бренду.

SERM от AdvertPro – это не просто ваш личный инструмент для укрепления положительного имиджа вашей компании в интернете. Благодаря нашей системы, вы получите полное управление над тем, что рассказывают о вашем бизнесе люди. SERM просматривает онлайн-упоминания и работает на усиление позитивных отзывов, в то же время уменьшая влияние негатива. Мы используем современные алгоритмы поиска, чтобы вы были на шаг впереди конкурентов.

Представьте себе, что каждый поиск о вашей компании направляет к позитивным отзывам: лестные отзывы, убедительные кейсы успешных операций и отличные рекомендации. С SERM от AdvertPro это не просто мечта, находящаяся в пределах досягаемости каждому предприятию. Более того, наш инструмент дает возможность получить ценной обратной связью для совершенствования вашего сервиса.

Используйте возможность укрепить свою деловую репутацию. Обратитесь к нам прямо сейчас для запроса профессиональной консультации и запуска сервиса SERM. Дайте возможность миллионам потенциальных клиентов узнавать только с лучшим о вашем бизнесе каждый раз, когда они ищут в интернет за информацией. Откройте новую страницу в управлении онлайн-репутацией – выберите AdvertPro!

Сайт: [url=https://serm-moscow.ru/]заказать управление репутацией фирмы.[/url]

Теория внутреннего стимулирования лидерства. Тип политического лидерства. Поведенческое лидерство. Сетевое лидерство это. Лидерство картинки. Функции политического лидерства.

онлайн

Смотреть фильмы онлайн. Фильмы онлайн — сайт. Смотреть онлайн-кинотеатры. Фильмы смотреть онлайн бесплатно в HD1080. Легально ли смотреть фильмы онлайн? Смотреть фильмы онлайн бесплатно без регистрации. Фильмы и сериалы смотреть онлайн бесплатно.

Xanax – Your partner in tackling anxiety. Learn how Buy Xanax for Quick Stress Control can assist you in finding peace of mind. Start your path to relief now.

Смотреть фильмы онлайн бесплатно в хорошем качестве. Смотреть фильмы / топ кино онлайн. Смотреть фильмы онлайн бесплатно в хорошем HD качестве. Смотреть фильмы в хорошем качестве (HD, 1080p) в онлайн. Смотреть фильмы онлайн бесплатно в хорошем качестве. Новинки уже вышедшие смотреть онлайн в хорошем качестве.

https://tinyurl.com/ylpmzbb5

смотреть

Смотреть онлайн фильмы и сериалы бесплатно. Фильмы онлайн в хорошем качестве без рекламы. Лучший онлайн-кинотеатр советских фильмов. Сериалы онлайн, смотреть онлайн бесплатно. Все части кино смотреть онлайн в хорошем качестве hd 1080. Смотреть Аниме онлайн бесплатно в хорошем качестве. Сериалы онлайн смотреть бесплатно в хорошем качестве. Смотреть аниме онлайн в хорошем качестве HD бесплатно.

https://tinyurl.com/ypqoj973

Смотреть фильмы в хорошем качестве (HD, 1080p) в онлайн. Смотреть фильмы онлайн бесплатно в хорошем качестве. Новинки уже вышедшие смотреть онлайн в хорошем качестве. Смотреть фильмы онлайн в хорошем качестве Full HD 720. Смотреть фильмы онлайн в хорошем качестве бесплатно. Фильмы смотреть онлайн в хорошем качестве. Смотреть фильмы онлайн в хорошем качестве. Список лучших.

Бесплатные фильмы смотреть онлайн в хорошем качестве. Смотреть фильмы в хорошем качестве (HD, 1080p) в онлайн. Смотреть онлайн фильмы и сериалы. Смотреть фильмы онлайн в хорошем качестве бесплатно. Смотреть фильмы онлайн. Фильмы смотреть онлайн.

Новые фильмы смотреть онлайн бесплатно в хорошем качестве. Смотрите фильмы в отличном качестве без регистрации! Смотреть фильмы в онлайн кинотеатре в хорошем качестве. Совместный просмотр фильмов: список сайтов и сервисов. ФИЛЬМЫ ОНЛАЙН БЕСПЛАТНО. Смотреть фильмы онлайн в хорошем качестве.

Фильмы и сериалы онлайн смотреть онлайн. Смотреть фильмы в хорошем качестве (HD, 1080p) в онлайн. Смотреть фильмы онлайн бесплатно в хорошем качестве. Смотреть новые фильмы онлайн, которые уже вышли. Новинки. Смотреть фильмы онлайн. Фильмы онлайн смотреть онлайн. Смотреть фильмы онлайн в хорошем качестве Full HD 720. Фильмы – смотреть онлайн бесплатно в хорошем качестве.

民調

民意調查是什麼?民調什麼意思?

民意調查又稱為輿論調查或民意測驗,簡稱民調。一般而言,民調是一種為了解公眾對某些政治、社會問題與政策的意見和態度,由專業民調公司或媒體進行的調查方法。

目的在於通過網路、電話、或書面等媒介,對大量樣本的問卷調查抽樣,利用統計學的抽樣理論來推斷較為客觀,且能較為精確地推論社會輿論或民意動向的一種方法。

以下是民意調查的一些基本特點和重要性:

抽樣:由於不可能向每一個人詢問意見,所以調查者會選擇一個代表性的樣本進行調查。這樣本的大小和抽樣方法都會影響調查的準確性和可靠性。

問卷設計:為了確保獲得可靠的結果,問卷必須經過精心設計,問題要清晰、不帶偏見,且易於理解。

數據分析:收集到的數據將被分析以得出結論。這可能包括計算百分比、平均值、標準差等,以及更複雜的統計分析。

多種用途:民意調查可以用於各種目的,包括政策制定、選舉預測、市場研究、社會科學研究等。

限制:雖然民意調查是一個有價值的工具,但它也有其限制。例如,樣本可能不完全代表目標人群,或者問卷的設計可能導致偏見。

影響決策:民意調查的結果常常被政府、企業和其他組織用來影響其決策。

透明度和誠實:為了維護調查的可信度,調查組織應該提供其調查方法、樣本大小、抽樣方法和可能的誤差範圍等詳細資訊。

民調是怎麼調查的?

民意調查(輿論調查)的意義是指為瞭解大多數民眾的看法、意見、利益與需求,以科學、系統與公正的資料,蒐集可以代表全部群眾(母體)的部分群眾(抽樣),設計問卷題目後,以人工或電腦詢問部分民眾對特定議題的看法與評價,利用抽樣出來部分民眾的意見與看法,來推論目前全部民眾的意見與看法,藉以衡量社會與政治的狀態。

以下是進行民調調查的基本步驟:

定義目標和目的:首先,調查者需要明確調查的目的。是要了解公眾對某個政策的看法?還是要評估某個政治候選人的支持率?

設計問卷:根據調查目的,研究者會設計一份問卷。問卷應該包含清晰、不帶偏見的問題,並避免導向性的語言。

選擇樣本:因為通常不可能調查所有人,所以會選擇一部分人作為代表。這部分人被稱為“樣本”。最理想的情況是使用隨機抽樣,以確保每個人都有被選中的機會。

收集數據:有多種方法可以收集數據,如面對面訪問、電話訪問、郵件調查或在線調查。

數據分析:一旦數據被收集,研究者會使用統計工具和技術進行分析,得出結論或洞見。

報告結果:分析完數據後,研究者會編寫報告或發布結果。報告通常會提供調查方法、樣本大小、誤差範圍和主要發現。

解釋誤差範圍:多數民調報告都會提供誤差範圍,例如“±3%”。這表示實際的結果有可能在報告結果的3%範圍內上下浮動。

民調調查的質量和可信度很大程度上取決於其設計和實施的方法。若是由專業和無偏見的組織進行,且使用科學的方法,那麼民調結果往往較為可靠。但即使是最高質量的民調也會有一定的誤差,因此解讀時應保持批判性思考。

為什麼要做民調?

民調提供了一種系統性的方式來了解大眾的意見、態度和信念。進行民調的原因多種多樣,以下是一些主要的動機:

政策制定和評估:政府和政策制定者進行民調,以了解公眾對某一議題或政策的看法。這有助於制定或調整政策,以反映大眾的需求和意見。

選舉和政治活動:政黨和候選人通常使用民調來評估自己在選舉中的地位,了解哪些議題對選民最重要,以及如何調整策略以吸引更多支持。

市場研究:企業和組織進行民調以了解消費者對產品、服務或品牌的態度,從而制定或調整市場策略。

社會科學研究:學者和研究者使用民調來了解人們的社會、文化和心理特征,以及其與行為的關係。

公眾與媒體的期望:民調提供了一種方式,使公眾、政府和企業得以了解社會的整體趨勢和態度。媒體也經常報導民調結果,提供公眾對當前議題的見解。

提供反饋和評估:無論是企業還是政府,都可以透過民調了解其表現、服務或政策的效果,並根據反饋進行改進。

預測和趨勢分析:民調可以幫助預測某些趨勢或行為的未來發展,如選舉結果、市場需求等。

教育和提高公眾意識:通過進行和公布民調,可以促使公眾對某一議題或問題有更深入的了解和討論。

民調可信嗎?

民意調查的結果數據隨處可見,尤其是政治性民調結果幾乎可說是天天在新聞上放送,對總統的滿意度下降了多少百分比,然而大家又信多少?

在景美市場的訪問中,我們了解到民眾對民調有一些普遍的觀點。大多數受訪者表示,他們對民調的可信度存有疑慮,主要原因是他們擔心政府可能會在調查中進行操控,以符合特定政治目標。

受訪者還提到,民意調查的結果通常不會對他們的投票意願產生影響。換句話說,他們的選擇通常受到更多因素的影響,例如候選人的政策立場和政府做事的認真與否,而不是單純依賴民調結果。

從訪問中我們可以得出的結論是,大多數民眾對民調持謹慎態度,並認為它們對他們的投票決策影響有限。

Хостинг Windows VDS / VPS серверов

– Супер (аптайм, скорость, пинг, нагрузка)

– Windows – 2012 R2, 2016, 2019, 2022 – бесплатно

– Отлично подходит под CapMonster

– Почасовая оплата

– Ubuntu, Debian, CentOS, Oracle 9 – бесплатно

– Дата-центр в Москве и Амстердаме

– Отлично подходит под XRumer + XEvil

– Быстрые серверы с NVMe.

– Отлично подходит под A-Parser

– Управляйте серверами на лету.

– Windows – 2022, 2019, 2016, 2012 R2

– Outline VPN, WireGuard VPN, IPsec VPN.

– Автоматическая установка Windows – бесплатно

– Возможность арендовать сервер на 1 час или 1 сутки

– Для сервера сеть на скорости 1 Гбит!

– Более 15 000 сервер уже в работе

– FASTPANEL и HestiaCP – бесплатно

– Круглосуточная техническая поддержка – бесплатно

– Отлично подходит под Xneolinks

– Мгновенное развёртывание сервера в несколько кликов – бесплатно

– Отлично подходит под GSA Search Engine Ranker

– Скорость порта подключения к сети интернет — 1000 Мбит/сек

Аренда виртуальных серверов (VPS/VDS хостинг)

– Автоматическая установка Windows – бесплатно

– Отлично подходит под CapMonster

– Ubuntu, Debian, CentOS, Oracle 9 – бесплатно

– Возможность арендовать сервер на 1 час или 1 сутки

– Отлично подходит под A-Parser

– Отлично подходит под GSA Search Engine Ranker

– Отлично подходит под Xneolinks

– Более 15 000 сервер уже в работе

– Windows – 2022, 2019, 2016, 2012 R2

– Windows – 2012 R2, 2016, 2019, 2022 – бесплатно

– Супер (аптайм, скорость, пинг, нагрузка)

– Управляйте серверами на лету.

– Отлично подходит под XRumer + XEvil

– FASTPANEL и HestiaCP – бесплатно

– Для сервера сеть на скорости 1 Гбит!

– Дата-центр в Москве и Амстердаме

– Почасовая оплата

– Быстрые серверы с NVMe.

– Скорость порта подключения к сети интернет — 1000 Мбит/сек

– Мгновенное развёртывание сервера в несколько кликов – бесплатно

– Круглосуточная техническая поддержка – бесплатно

– Outline VPN, WireGuard VPN, IPsec VPN.

Аренда VDS или VPS сервера

– Почасовая оплата

– Скорость порта подключения к сети интернет — 1000 Мбит/сек

– FASTPANEL и HestiaCP – бесплатно

– Дата-центр в Москве и Амстердаме

– Отлично подходит под CapMonster

– Мгновенное развёртывание сервера в несколько кликов – бесплатно

– Возможность арендовать сервер на 1 час или 1 сутки

– Автоматическая установка Windows – бесплатно

– Круглосуточная техническая поддержка – бесплатно

– Outline VPN, WireGuard VPN, IPsec VPN.

– Ubuntu, Debian, CentOS, Oracle 9 – бесплатно

– Быстрые серверы с NVMe.

– Отлично подходит под A-Parser

– Отлично подходит под Xneolinks

– Отлично подходит под XRumer + XEvil

– Супер (аптайм, скорость, пинг, нагрузка)

– Управляйте серверами на лету.

– Windows – 2012 R2, 2016, 2019, 2022 – бесплатно

– Более 15 000 сервер уже в работе

– Для сервера сеть на скорости 1 Гбит!

– Windows – 2022, 2019, 2016, 2012 R2

– Отлично подходит под GSA Search Engine Ranker

VPS VDS на Windows

– Отлично подходит под CapMonster

– Отлично подходит под XRumer + XEvil

– Скорость порта подключения к сети интернет — 1000 Мбит/сек

– Windows – 2012 R2, 2016, 2019, 2022 – бесплатно

– Outline VPN, WireGuard VPN, IPsec VPN.

– Отлично подходит под A-Parser

– Почасовая оплата

– Супер (аптайм, скорость, пинг, нагрузка)

– Дата-центр в Москве и Амстердаме

– Управляйте серверами на лету.

– Ubuntu, Debian, CentOS, Oracle 9 – бесплатно

– Быстрые серверы с NVMe.

– Более 15 000 сервер уже в работе

– Отлично подходит под GSA Search Engine Ranker

– Windows – 2022, 2019, 2016, 2012 R2

– FASTPANEL и HestiaCP – бесплатно

– Круглосуточная техническая поддержка – бесплатно

– Для сервера сеть на скорости 1 Гбит!

– Отлично подходит под Xneolinks

– Возможность арендовать сервер на 1 час или 1 сутки

– Мгновенное развёртывание сервера в несколько кликов – бесплатно

– Автоматическая установка Windows – бесплатно

смотреть

https://tinyurl.com/ytz6u9to

https://tinyurl.com/ytmauk3v

https://tinyurl.com/yoxoko6f

Аренда VPS и VDS сервера – Dedicated Server

– Возможность арендовать сервер на 1 час или 1 сутки

– Быстрые серверы с NVMe.

– Windows – 2012 R2, 2016, 2019, 2022 – бесплатно

– Ubuntu, Debian, CentOS, Oracle 9 – бесплатно

– Outline VPN, WireGuard VPN, IPsec VPN.

– Супер (аптайм, скорость, пинг, нагрузка)

– Почасовая оплата

– Управляйте серверами на лету.

– Для сервера сеть на скорости 1 Гбит!

– Более 15 000 сервер уже в работе

– Мгновенное развёртывание сервера в несколько кликов – бесплатно

– Дата-центр в Москве и Амстердаме

– Windows – 2022, 2019, 2016, 2012 R2

– Отлично подходит под A-Parser

– Отлично подходит под CapMonster

– Круглосуточная техническая поддержка – бесплатно

– Автоматическая установка Windows – бесплатно

– FASTPANEL и HestiaCP – бесплатно

– Отлично подходит под GSA Search Engine Ranker

– Скорость порта подключения к сети интернет — 1000 Мбит/сек

– Отлично подходит под XRumer + XEvil

– Отлично подходит под Xneolinks

сериал

https://tinyurl.com/yrtb3d8m

онлайн

https://tinyurl.com/ywhu3blv

Здравствуйте, ценные предприниматели, представляем вам вашему вниманию прогрессивный продукт от AdvertPro – SERM (Search Engine Reputation Management), систему управления репутацией в сети Интернет! В цифровом мире, репутация в интернете имеет важную роль в успехе вашего бизнеса. Не позволяйте, чтобы неконтролируемые отзывы и непонимания повредили доверию к вашему бренду.

SERM от AdvertPro – это более чем ваш личный инструмент для укрепления положительного имиджа вашей компании в интернете. С помощью нашей системы, вы обретете полное управление над тем, что писают о вашем бизнесе ваши клиенты. SERM отслеживает онлайн-упоминания и способствует распространению позитивных отзывов, одновременно уменьшая влияние негатива. Мы применяем современные алгоритмы поиска, чтобы вы были на шаг впереди своих конкурентов.

Вообразите, что каждый поиск о вашей компании направляет к положительным результатам: позитивные комментарии, убедительные кейсы успешных операций и отличные рекомендации. С SERM от AdvertPro это реальность, доступная всем компаниям. Более того, наш инструмент предоставляет возможность получить ценной обратной связью для усовершенствования вашего бизнеса.

Не теряйте возможность укрепить свою деловую репутацию. Обратитесь к нам прямо сейчас для запроса профессиональной консультации и начните использовать SERM. Позвольте миллионам потенциальных клиентов узнавать только с лучшим о вашем бизнесе каждый раз, когда они заглядывают в интернет за информацией. Начните новую страницу в управлении онлайн-репутацией – выберите AdvertPro!

Сайт: [url=https://serm-moscow.ru/]репутация компании в сети интернет.[/url]

Друзья нуждались в поддержке, и я решил подарить им цветы. “Цветов.ру” сделал этот процесс простым, а красочный букет точно придал им немного света в серых буднях. Советую! Вот ссылка [url=https://mscs-boost.ru/yola/]заказать цветы с доставкой[/url]

Друзья нуждались в поддержке, и я решил подарить им цветы. “Цветов.ру” сделал этот процесс простым, а красочный букет точно придал им немного света в серых буднях. Советую! Вот ссылка [url=https://acter-sochi-sanatoriy.ru/orenburg/]заказать букет с доставкой[/url]

Сделал нелепую ошибку и решил ее исправить. Купил на “Цветов.ру” восхитительный букет, чтобы передать свои извинения. Ребята, сервис просто волшебен – быстро, удобно, и цветы свежайшие! Советую! Вот ссылка [url=https://ushtirlitsa.ru/chel/]магазин цветов[/url]

44738

фильм в хорошем качестве

60575

Ad usum externum — Для внешнего употребления.

http://batmanapollo.ru

сериал 2024

Amabilis insania — Приятное безумие.

http://batmanapollo.ru

Cognata vocabula rebus — Слова, соответствующие поступкам

http://batmanapollo.ru

GGpokerOK

ПокерОк

С того дня, как я начал правильно питаться, моя жизнь изменилась. Я благодарю компанию ‘все соки’ за их [url=https://blender-bs5.ru/collection/sokovyzhimalki-dlya-granata]соковыжималку для граната[/url]. Теперь каждое утро начинается с бодрящего гранатового сока!

Решение купить шнековую соковыжималку изменило моё представление о здоровом питании. Благодарю ‘Все соки’ за их чудесную продукцию. Их [url=https://blender-bs5.ru/collection/ruchnye-shnekovye-sokovyzhimalki]шнековая соковыжималка купить[/url] оказалась лучшим вложением в моё здоровье.

Решение купить соковыжималку для овощей и фруктов было ключевым моментом в моем пути к здоровому образу жизни. ‘Все соки’ предложили отличный выбор. [url=https://h-100.ru/collection/sokovyzhimalki-dlja-ovoshhej-fruktov]Купить соковыжималку для овощей и фруктов[/url] от ‘Все соки’ было лучшим решением для моего здоровья!

psyho2031.8ua.ru

psyho2031.8ua.ru

psyho2031.8ua.ru

psyho2031.8ua.ru

psyho2031.8ua.ru

psyho2031.8ua.ru

psyho2031.8ua.ru

PokerOK

ggpokerok официальный сайт

Мастер и Маргарита 2024

Андрей Фролов, отличившийся на экономическом факультете МГУ, проявил себя как одаренный финансист в крупном банке. Его карьерный рост был обусловлен не только профессионализмом, но и способностью к нестандартному мышлению в сложных финансовых ситуациях. Сейчас Андрей применяет свои навыки для анализа рынка и разработки инвестиционных стратегий на mikro-zaim-online.ru, обеспечивая клиентам выгодные условия займов. Подробнее о нем и о предложениях займов можно узнать на https://mikro-zaim-online.ru/o-nas/

http://psyho2039.8ua.ru/

http://psyho2039.8ua.ru/

http://psyho2039.8ua.ru/

Thanks-a-mundo for the post.Really thank you! Awesome.

My website: русское порно учитель

рейтинг онлайн казино 2024

https://l2db.com.ua

Легальні казино в Україні стають важливим аспектом розвитку гральної індустрії у країні. Законодавчі зміни в останні роки створили сприятливе середовище для розвитку онлайн та оффлайн гральних закладів. Існують декілька ключових факторів, які роблять легальні казино в Україні привабливими для гравців та інвесторів.

Однією з основних переваг є регулювання грального бізнесу державою, що гарантує чесність та безпеку для гравців. Легальність казино в Україні відображається в ретельних перевірках та ліцензіях, які видаються органами влади. Це забезпечує гравцям впевненість у тому, що їхні фінансові та особисті дані захищені.

Завдяки інноваційним технологіям, легальні казино в Україні швидко адаптуються до потреб гравців. Онлайн-платформи надають можливість грати в улюблені азартні ігри зручно та безпечно прямо з дому чи мобільного пристрою. Завдяки високій якості графіки та захоплюючому геймплею, гравці можуть насолоджуватися атмосферою класичних казино в будь-якому місці та в будь-який час.

Партнерські програми та бонуси, що пропонують легальні казино в Україні, роблять гру ще більш привабливою для новачків. Інколи це може включати в себе бездепозитні бонуси, фріспіни або інші ексклюзивні пропозиції для реєстрації. Гравець може отримати додатковий стимул для гри та виграшу, що робить гральний процес ще захопливішим.

Легальні казино в Україні також сприяють розвитку туризму, приваблюючи гравців з інших країн. Вони стають місцем для соціальних подій, турнірів та розваг, що сприяє позитивному іміджу країни та збільшенню її привабливості для іноземних туристів.

У світі розваг та азарту, легальні казино в Україні виступають як підтримуючий стовп розвитку економіки. Збалансована політика та тісне співробітництво між гральними операторами та державними органами сприяють позитивному розвитку цієї індустрії. Гравці отримують можливість насолоджуватися азартом в безпечному та легальному середовищі, що робить казино в Україні привабливим вибором для всіх шанувальників азартних розваг.

Definitely, what a great blog and revealing posts, I definitely will bookmark your site. Best Regards!

My website: порно массажист

Wohh precisely what I was searching for, regards for putting up.

My website: российское порно

A lot of blog writers nowadays yet just a few have blog posts worth spending time on reviewing.

My website: порно студентки русское

Muchos Gracias for your article.Really thank you! Cool.

My website: порно масаж

https://bit.ly/sistemniy-podkhod

https://bit.ly/sistemniy-podkhod

https://bit.ly/sistemniy-podkhod

https://bit.ly/sistemniy-podkhod

https://bit.ly/sistemniy-podkhod

https://bit.ly/sistemniy-podkhod

https://bit.ly/sistemniy-podkhod

I got what you intend,bookmarked, very decent website.

My website: порно изнасилование онлайн

морг института склифосовского http://www.ritual-gratek20.ru/.

Thanks for sharing, this is a fantastic blog post.Really thank you! Much obliged.

My website: порно реальный массаж

I reckon something truly special in this website.

My website: лучший анальный секс

https://prodvizheniekontekstnayareklama.ru

Thank you ever so for you blog. Really looking forward to read more.

My website: порно русских подростков

My website: порнуха с мамой

онлайн

сериал онлайн

сериал бесплатно

сериал онлайн

https://kupitkvartiruzhkkvartirenka.ru

https://kupitkvartiruzhkgarsonerka.ru

https://referatyrimskoepravo.ru

Join the fun at our Mexican online casino and discover why we’re the hottest destination for players seeking big wins and non-stop entertainment. jugar casino en vivo la clave para una vida lujosa.

https://kupitkvartiruland.ru

https://referatyrusskijyazyk.ru

https://kontrolnyestatistika.ru

https://referatystatistika.ru

This piece truly showcases the critical nature of the matter at hand, offering insightful perspectives that resonate with a vast readership. For more comprehensive data, feel free to browse new’s. It’s especially refreshing to witness such captivating dialogues that spark meaningful engagement across diverse disciplines.

https://kontrolnyepravovedenie.ru

This piece truly illuminates the vital nature of the topic at hand, offering perceptive observations that strike a chord with a vast audience. For more thorough data, feel free to explore https://ur9d9w107r4.typeform.com/to/BZu6psMR. It’s uniquely revitalizing to witness such engaging exchanges that kindle insightful dialogue across multiple fields.

https://resheniezadachpolitologiya.ru

This entry truly highlights the essential nature of the topic at hand, offering insightful perspectives that resonate with a vast readership. For additional comprehensive insight, feel free to visit https://ur9d9w107r4.typeform.com/to/BZu6psMR. It’s remarkably stimulating to witness such fascinating dialogues that stimulate insightful dialogue across a multitude of areas.

Win big and live the dream at our Mexican online casino. With life-changing jackpots and thrilling tournaments, fortune favors the bold. codere casino online la clave para una buena vida.

Thank you ever so for you blog. Really looking forward to read more.

My website: сперма в пизде

https://resheniezadachlogika.ru/

This article truly exposes the vital importance of the subject at hand, offering astute views that strike a chord with a broad readership. For further comprehensive insight, feel free to visit https://ur9d9w107r4.typeform.com/to/BZu6psMR. It’s remarkably revitalizing to witness such compelling exchanges that spark thoughtful conversation across multiple fields.

Respect to post author, some fantastic information

My website: секс по казахскии

This piece truly showcases the paramount importance of the matter at hand, offering perceptive observations that strike a chord with a wide public. For extended comprehensive insight, feel free to check out https://www.homeoffice.com.pl/. It’s especially stimulating to witness such engaging conversations that ignite profound dialogue across diverse disciplines.

https://resheniezadachmarketing.ru/

I’m extremely pleased to discover this website. I wanted to thank you for ones time just for this fantastic read!

My website: русский пьяный секс видео

Win big and live the dream at our Mexican online casino. With life-changing jackpots and thrilling tournaments, fortune favors the bold. casion la clave para una buena vida.

This contribution truly highlights the essential importance of the matter at hand, offering astute perspectives that resonate with a vast public. For additional in-depth data, feel free to explore https://www.homeoffice.com.pl/. It’s remarkably invigorating to witness such engaging exchanges that stimulate thoughtful conversation across diverse fields.

This piece truly highlights the paramount importance of the matter at hand, offering shrewd observations that resonate with a broad audience. For extended comprehensive information, feel free to browse new’s. It’s particularly invigorating to witness such engaging dialogues that spark profound engagement across a multitude of domains.

This entry truly illuminates the paramount nature of the subject at hand, offering insightful views that strike a chord with a diverse audience. For further thorough data, feel free to browse new’s. It’s especially invigorating to witness such compelling exchanges that kindle meaningful conversation across diverse fields.

This article truly exposes the vital nature of the matter at hand, offering astute observations that echo with a wide public. For more detailed information, feel free to explore new’s. It’s especially invigorating to witness such captivating conversations that ignite insightful interaction across diverse domains.

This article truly showcases the critical essence of the subject at hand, offering astute insights that strike a chord with a wide readership. For additional thorough insight, feel free to browse new’s. It’s remarkably refreshing to witness such captivating discussions that spark meaningful engagement across multiple disciplines.

https://tekhnicheskiy-perevod.ru/

купить аттестат школы https://www.arusak-diploms.com .

This post was an informative read, offering a profound understanding of the issue. Your ability to delve into complex matters and present them in an comprehensible manner is truly praiseworthy. I’m eager to see what topics you will discuss next. For more perspectives, I encourage everyone to visit https://keyoftech.ovh/.

This article was an illuminating read, offering a deep understanding of the theme. Your ability to investigate complex subjects and present them in an comprehensible manner is truly laudable. I’m keen to see what topics you will address next. For more details, I encourage everyone to visit https://keyoftech.ovh/.

This entry was an enlightening read, offering a deep understanding of the subject matter. Your ability to delve into complex issues and present them in an accessible manner is truly laudable. I’m anxious to see what topics you will tackle next. For more insights, I encourage everyone to visit https://keyoftech.ovh/.

This piece was an illuminating read, offering a profound understanding of the theme. Your ability to examine complex matters and present them in an comprehensible manner is truly laudable. I’m keen to see what areas you will discuss next. For more information, I encourage everyone to visit https://keyoftech.ovh/.

https://kursovyesociologiya.ru/

Thank you ever so for you blog. Really looking forward to read more.

My website: смотреть арабское порно